You Haven’t Completed M&A Due Diligence Until You Know a Target’s Material Margin

Many put too much emphasis on gross margin when it can lie and not...

Read More

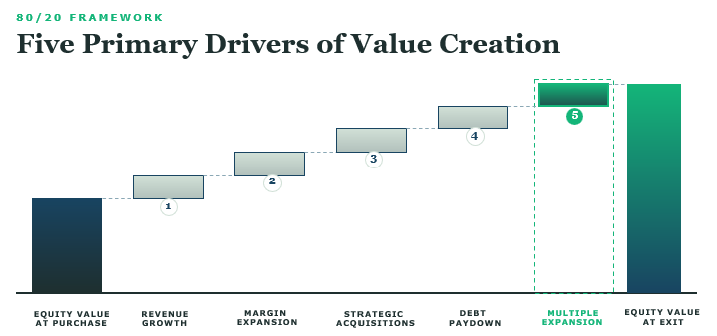

80/20 gives lower-middle-market management teams a repeatable way to cut through complexity and act on what actually drives results. Learn how the 80/20 framework is a proven approach to attacking all five drivers of value creation.

According to a recent analysis of more than 10,000 global PE investments, revenue growth and margin expansion together account for 68% of value creation in PE-backed companies, with multiple expansion contributing just 32%.[1] That's a dramatic shift from 2019-2021, when multiple expansion alone drove nearly half of returns.[2] Revenue growth and margin improvement have to make up the difference.

This means portfolio companies have to get better. But most are running dozens of initiatives with limited management bandwidth and compressed timelines. Everything is a priority, so nothing is. 80/20 is the fix. Most people think of it as a productivity hack or a cocktail-party line about 80% of results coming from 20% of inputs. But it's a diagnostic tool that shows where value lives in a business and how to compound it.

Here is how 80/20 actions map directly to the five primary drivers of value creation.

Most B2B companies have significant revenue concentration. 20% of customers generate 80% of revenue. 20% of products account for 80% of revenue. 20% of sales reps deliver 80% of new business. This isn't a weakness; it's a pattern to exploit.

But most companies don't. They treat all customers like they're equally valuable. Same service model. Same sales coverage. Same process for creating a quote, making a widget, and shipping it. Same pricing discipline. It's egalitarian. It's also wildly inefficient.

An industrial distributor had $45M in revenue across 2,300 customers. The top 150 customers (6%) generated $28M at a 42% gross margin, with 95% retention. The bottom 1,800 customers generated $8M at 18% margin and churned at 35% annually. Shockingly, the company spent more time and effort serving the 1,800 than it did serving the top 150, which conservatively generated 150% of EBITDA.

In one year, the company grew revenue from $45M to $54M and gross profit from $13M to $20M, a 46% increase. Nearly all of that growth came from expanding wallet share with existing high-value customers. They refocused their best sales reps on key account management and built a tiered service model that delivered a fundamentally different and better experience to the top 150 customers. The long tail got pushed to e-commerce and self-service.

The insight: you don't need more customers. You need to stop treating your best ones like everyone else. Elevate their customer experience, and profitable wallet share gains follow.

How many of your SKUs exist because someone asked for them once in 2017? How many legacy processes do you have that made sense when Clinton was president? B2B companies are complexity sponges. Every year, they add custom SKUs, set up one-time customers, run credit checks on companies that will never spend more than $100, and spend countless hours on contract edits for customers that will make a one-time buy for less than it costs to review the documents. It’s death by a thousand accommodations.

Margin expansion in PE-backed companies usually means procurement squeezes and headcount cuts. Fine. Those are one-time gains that make the model happy. But the sustainable path to margin expansion is complexity reduction by eliminating the products, services, and processes that consume disproportionate resources and destroy value.

A specialty chemicals company with $80M in revenue and 1,200 SKUs had flat margins despite volume growth. An 80/20 analysis showed that 180 SKUs (15%) generated 75% of revenue and 85% of gross profit. The bottom 600 SKUs generated 4% of revenue but consumed 30% of production changeover time and 40% of quality control resources.

Management re-priced the bottom 400 SKUs to reflect their true cost to serve, and they discontinued SKUs that didn't meet minimum volume thresholds after repricing. Over twelve months, the company eliminated 320 SKUs, expanded gross margins from 38% to 44%, and increased production throughput 18% without adding capacity.

The insight: Your customers don't want 1,000 SKUs. They want the 200 that create customer value, delivered on time and in full, with zero quality issues.

Most PE firms have a buy-and-build thesis. The problem is that most acquisitions create distraction rather than value because they combine two companies' long tails, integrate incompatible systems and cultures, try to become everything to everyone, and hope "scale" magically appears. It doesn't.

The 80/20 approach to add-ons starts with a simple question: do the target's 80s complement the platform's 80s? If the answer is yes, you're building on strength. If it's no, you're just mashing two complex blobs together, creating a value-destroying super-blob.

A commercial HVAC platform was evaluating two add-ons. Target A had $28M in revenue spread across 15 verticals. Target B had $10M, with 70% concentrated in healthcare and higher education, two segments where the platform was already strong. On paper, Target A looks like the obvious pick. But Target B's concentration is exactly what made it a better acquisition. Post-acquisition, cross-sell penetration in healthcare and higher-ed went from 22% to 41%, and revenue synergies exceeded underwriting by 60% in year one. Target A would have added more revenue and diluted focus.

The insight: Don’t buy companies just for the sake of getting bigger. Buy companies to get better at what you're already good at and corner your core markets.

Would you carry $4M in inventory to support $3M in revenue from customers who don't pay on time? That's not hypothetical; it was a client. The problem is that many profitable B2B companies are cash-inefficient because working capital is trapped in slow-moving inventory, extended payment terms for low-value customers, and collections processes that treat all receivables equally.

An industrial equipment distributor with $65M in revenue and $9M in EBITDA had only a 60% cash conversion. 80/20 revealed where the cash was hiding: 25% of SKUs accounted for 80% of turns, while the bottom 40% turned less than twice per year. The company was carrying $4M in inventory to support $3M in annual revenue from the bottom 30% of customers. On receivables, the top 20% of customers paid in 28 days, and the bottom 50% averaged 67 days.

In response, management reduced safety stock for slow-movers, implemented tiered payment terms, and prioritized collections by dollar value rather than invoice date. Over nine months, inventory declined from $9M to $6M, and DSO improved from 52 to 41 days. The combined impact freed up $4M in cash and accelerated deleveraging by nearly 6 months.

The insight: Working capital is a choice about who you're willing to finance, so make sure it is an investment in your most profitable customers and products.

Multiple expansion is partly market timing, but it's mostly about the quality of the business you're selling. Buyers pay premiums for businesses they understand and discount the ones they don't. That's what 80/20 does across a hold period: it makes the business story clearer and the risk profile lower.

An IT services provider had $22M in revenue across three service lines: custom development, staff augmentation, and managed services. 80/20 revealed that managed services, while just 35% of revenue, generated 65% of gross profit and had 95% annual retention versus 60% for the other lines.

Management doubled down on managed services and its higher-quality revenue, restricted custom development for existing managed services customers only, and wound down staff augmentation except for strategic accounts. Over a three-year hold, revenue grew from $22M to $34M, with managed services growing from $8M to $26M. Gross margins expanded from 42% to 58%. At exit, the business wasn't positioned as a generalist provider (4-6x EBITDA) but as a specialized partner (8-10x EBITDA). The company sold at 9.2x, a multiple expansion of 2.5 turns, adding $15M to enterprise value independent of EBITDA growth.

The insight: Multiple expansion is part luck, but the businesses that command premiums aren't lucky; they're focused.

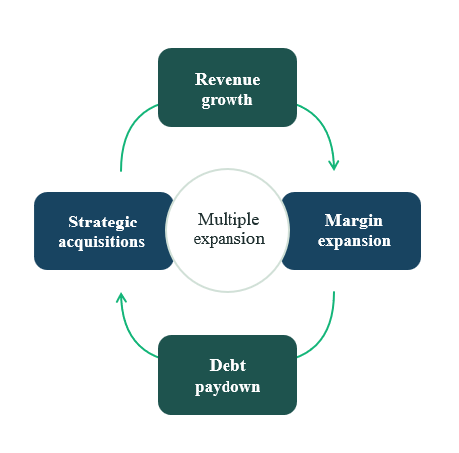

80/20 addresses each value creation driver on its own, but the gains compound. Revenue growth focused on high-value customers improves retention and wallet share, which improves margins. Margin expansion through complexity reduction frees up management bandwidth and improves cash conversion, which accelerates debt paydown. Strategic acquisitions that deepen core strengths make the platform story clearer. And when all five drivers are working together, that's what drives multiple expansion.

None of this requires new technology, massive capital investment, or wholesale management changes. All it requires is analytical rigor and the discipline to allocate resources where they'll actually create value, not where they're loudest or most visible.

For PE firms operating in the lower middle market, where portfolio companies often lack the infrastructure of larger businesses, 80/20 offers a pragmatic framework that management teams can execute. It's not a strategy; it's a lens for making better decisions faster.

Contact us to see how we can help your business today.

Never miss a beat. Get our latest insights in your inbox.